Credit assessment has always been at the center of lending decisions. For decades, banks and financial institutions relied on traditional credit evaluation methods such as credit scores, repayment history, and manual underwriting to determine borrower eligibility.

In 2026, Artificial Intelligence (AI) is changing this process significantly. Modern lenders are moving from static, rule-based systems toward AI-driven credit assessment models that use real-time financial data, predictive analytics, and automation.

The result is faster, smarter, and more inclusive lending decisions.

Table of Contents

What Is Traditional Credit Assessment?

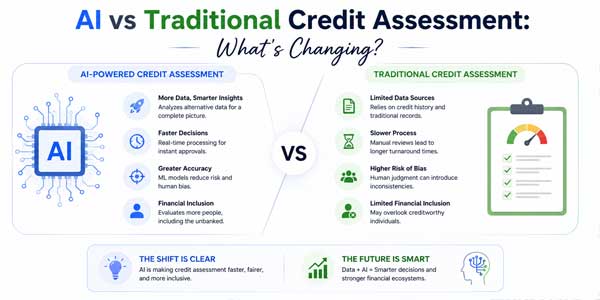

Traditional credit assessment evaluates a borrower’s ability to repay a loan using fixed financial indicators.

Common factors include:

- Credit score

- Loan repayment history

- Income statements

- Existing debt obligations

- Employment history

- Collateral value

Most traditional systems rely heavily on historical financial behavior and manual review processes.

While this method has worked for years, it also has limitations:

- Slow processing times

- Limited visibility into real-time financial health

- High manual effort

- Difficulty assessing thin-file borrowers

- Increased operational costs

What Is AI-Powered Credit Assessment?

AI-powered credit assessment uses machine learning and advanced analytics to evaluate borrower risk more dynamically.

Instead of relying only on credit scores, AI systems analyze:

- Cash flow patterns

- Bank transaction behavior

- Spending habits

- Business revenue trends

- Digital payment activity

- Alternative financial data

AI models continuously learn from historical and real-time data to improve prediction accuracy.

Key Differences Between AI and Traditional Credit Assessment

1.) Static Data vs Real-Time Financial Insights:

Traditional Assessment:

Traditional systems mainly depend on historical credit reports and past repayment records.

AI Assessment:

AI evaluates live financial behavior and ongoing cash flow patterns in real time.

This gives lenders a more updated and accurate picture of borrower risk.

2.) Manual Processing vs Automation:

Traditional Assessment:

Loan officers manually review applications, documents, and financial statements.

AI Assessment:

AI automates:

- Data extraction

- Risk scoring

- Document analysis

- Eligibility checks

- Fraud detection

This dramatically reduces approval times.

3.) Limited Credit Data vs Alternative Data Analysis:

Traditional Assessment:

Borrowers with limited credit history often struggle to qualify for loans.

AI Assessment:

AI can assess alternative data, such as:

- Utility payments

- Bank transactions

- E-commerce activity

- POS sales data

- Subscription payment history

This expands financial access for underserved borrowers and SMEs.

4.) Reactive Risk Models vs Predictive Intelligence:

Traditional Assessment

Traditional systems focus mainly on past borrower behavior.

AI Assessment

AI predicts future repayment risks using behavioral patterns and predictive analytics.

This helps lenders identify potential defaults earlier.

5.) Slower Decisions vs Instant Approvals:

Traditional Assessment

Loan approvals can take days or weeks due to manual verification processes.

AI Assessment

AI-driven systems can provide:

- Instant pre-qualification

- Automated approvals

- Real-time decisioning

This improves customer experience significantly.

6.) Human Error vs Data-Driven Accuracy:

Traditional Assessment:

Manual data entry and review increase the risk of errors and inconsistencies.

AI Assessment:

AI reduces operational mistakes through automated validation and intelligent analysis.

How AI Is Improving Credit Assessment?

Better Risk Evaluation:

AI models analyze broader financial patterns, improving accuracy in risk scoring.

Faster Lending Operations:

Automation accelerates underwriting and approval workflows.

Improved Fraud Detection:

AI identifies suspicious behavior, fake documents, and unusual financial activity earlier.

Financial Inclusion:

Borrowers without strong credit histories gain better access to financing opportunities.

Lower Operational Costs:

Banks and fintech companies reduce manual underwriting expenses.

Challenges of AI-Based Credit Assessment:

Despite its advantages, AI-powered credit assessment also presents challenges.

Data Privacy Concerns:

Financial institutions must handle sensitive customer data securely.

Bias in AI Models:

Poorly trained AI systems may unintentionally introduce bias into lending decisions.

Regulatory Compliance:

Lenders must ensure AI decisions remain transparent and explainable.

Integration Complexity:

Many traditional banks still operate on legacy infrastructure.

Industries Benefiting from AI Credit Assessment:

AI-powered credit assessment is growing across:

- Banking

- Fintech lending

- SME financing

- Mortgage lending

- Buy Now Pay Later (BNPL) platforms

- Commercial lending

Fintech companies, especially, are adopting AI rapidly to compete with traditional banks.

The Future of Credit Assessment:

The future of lending is becoming:

- More automated

- Real-time

- Predictive

- Personalized

- AI-driven

Human underwriters will still play an important role, but AI will increasingly handle routine credit evaluation tasks.

Agentic AI systems may soon manage entire lending workflows autonomously while humans focus on exceptions and compliance oversight.

Conclusion:

AI is transforming credit assessment from a slow, manual, and historically focused process into a dynamic, intelligent, and real-time system.

Compared to traditional credit assessment, AI offers:

- Faster approvals

- Better risk analysis

- Improved fraud detection

- Greater financial inclusion

- Lower operational costs

While challenges around transparency and regulation remain, AI-powered credit assessment is rapidly becoming the future standard for modern lending.

About the Author:

About the Author:Anand Subramanian at Intellectyx that is a leading AI and data engineering company helping financial institutions modernize lending workflows through intelligent automation. Specializing in AI for lending operations, Intellectyx builds advanced AI solutions for loan processing, borrower verification, credit assessment, fraud detection, and underwriting automation. The company helps banks, fintech firms, and financial service providers improve operational efficiency, accelerate approvals, and deliver smarter lending experiences with scalable AI-driven technologies.

Be the first to write a comment.